Irc 1031 Tax Free Exchange

What Is A 1031 Exchange Commercial Real Estate Md Va Dc

What Is A 1031 Exchange Asset Preservation Inc

1031 Exchange Rules Taking Advantage Of A 1031 Exchange In 2020 1031 Exchange Rules Squar Milner

1031 Exchanges By The Numbers Attorneys Cook Cook Commercial Real Estate Investing Exchange Financial Analysis

What S A 1031 Exchange And Why Does It Benefit Investors Nestiny Selling A Business Investing

Image Result For 1031 Exchange Ad Capital Gains Tax Things To Sell Investing

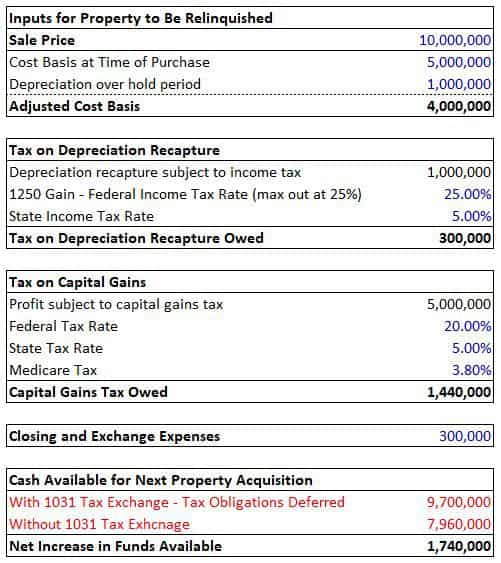

Generally have to pay tax on the gain at the time of sale.

Irc 1031 tax free exchange.

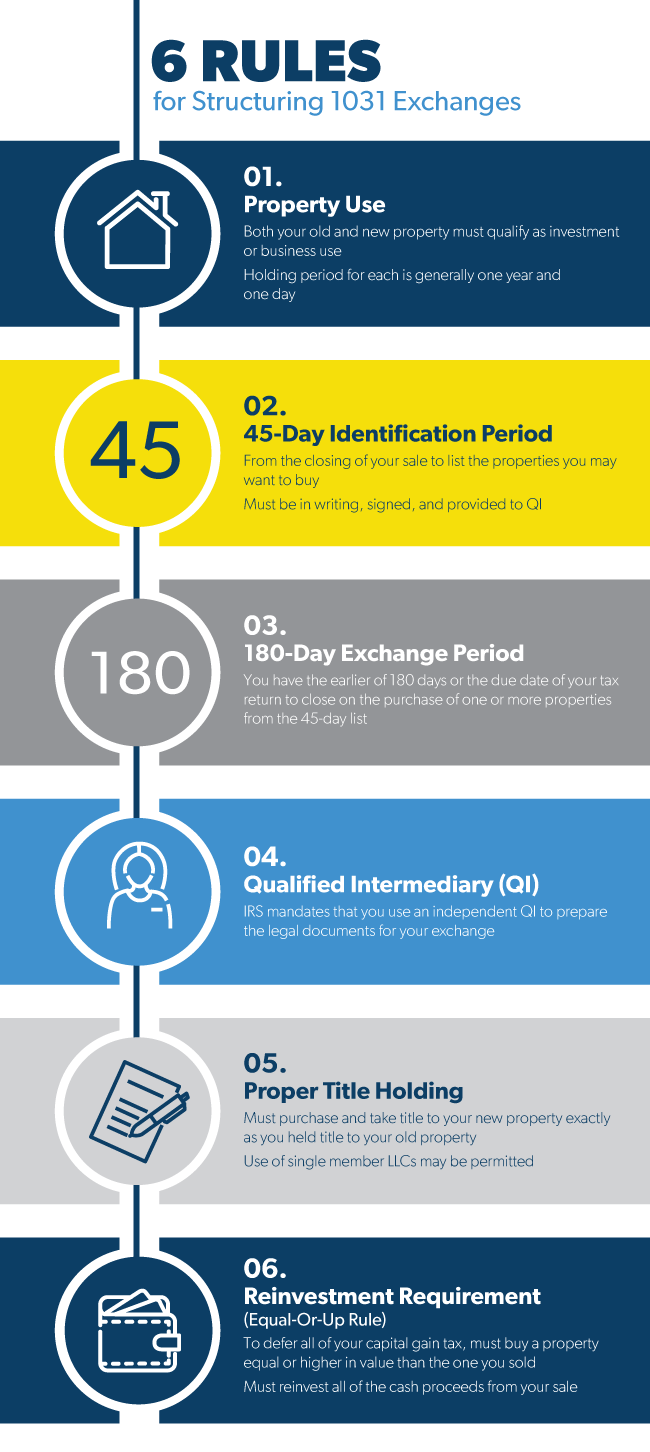

1031 Exchange Rules How To Do A 1031 Exchange

Replacing Debt In A 1031 Exchange Ipx1031

How To Do A 1031 Exchange Rules Definitions For Investors 2020

1031 Exchange Introduction Overview And Analysis Tool Adventures In Cre

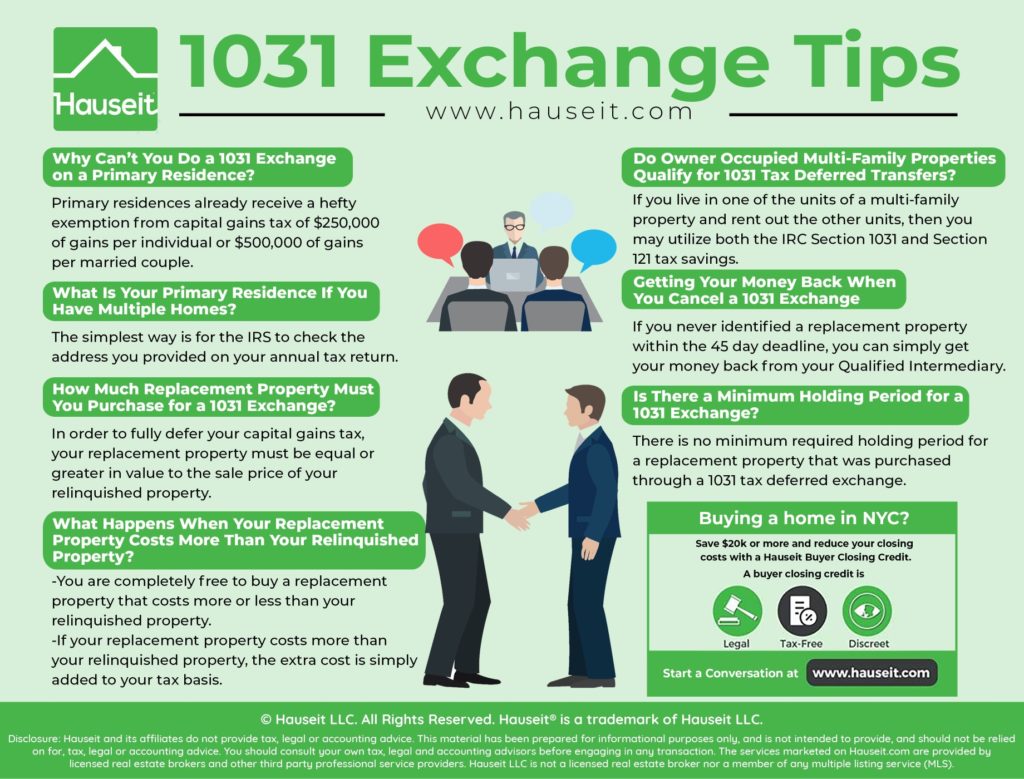

How To Do A 1031 Exchange In Nyc Hauseit New York City

Key Considerations In 1031 Exchanges With A Qualified Intermediary First American Exchange Company Exchange Consideration Company

Whats Is A 1031 Exchange Ash Mcginty Co

Rules For Converting Rental Property Into A Primary Residence Including After A 1031 Exchange And Claiming The Irc Section Rental Property Rental Residences

1031 Exchange And Primary Residence Asset Preservation Inc

All About 1031 Exchange Other Pins About This Also Real Estate Agent Florida Real Estate Realty

Pin On Benefit Of Irs Section 1031 Exchanges

Eight 1031 Exchange Rules You Can T Ignore Realtor Magazine Ignore Exchange Rules

How To Find The Right 1031 Exchange Property In 2020 Residential Real Estate Real Estate Investing Property

Frequently Asked Questions Faqs About 1031 Exchanges

Source : pinterest.com