Interest Rate Floor Spread

How Interest Rate Floors Work Finance Train

A Natural Floor On Corporate Spreads With Images Corporate Bonds Corporate Natural Flooring

Compounding Interest Rate Chart Interest Rate Chart Financial Charts Investing

Rising Mortgage Interest Rates With Images Mortgage Interest Rates Mortgage Rates Fixed Rate Mortgage

How Do Lower Mortgage Rates Affect Your Buying Power Mortgage Rates Interest Rates Stuff To Buy

:max_bytes(150000):strip_icc()/HowToReadInterestRateSwapQuotes1_4-ee013a308ef948ecb3ed106d6259a3f0.png)

How To Read Interest Rate Swap Quotes

Similarly an interest rate floor is a derivative contract in which the buyer receives payments at the end.

Interest rate floor spread.

Priced Out Of Moving Up In 2018 This Spring The Same Monthly Budget Can Buy 25 000 More House In 2020 Mortgage Rates Mortgage Monthly Budget

Fixed Indexed Annuities Fias 101 Fiainsights Org Value Stocks Annuity Stock Market Index

:max_bytes(150000):strip_icc()/GettyImages-180734345-ec5247651d704f57a7117eee952be492.jpg)

Interest Rate Floor Definition

Interest Only Mortgage Definition Interest Only Mortgage Interest Only Loan Mortgage

:max_bytes(150000):strip_icc()/dotdash_Final_Swap_Spread_Apr_2020-01-9ff4068939e742ca9cc066d6d7d481b3.jpg)

Swap Spread Definition

Sdvbwdzw6qu Am

Home Loans Interest Rates Create A Space Of Your Own With Hdfc Home Loans Best Housing Loan Interest Rates For Loan Interest Rates Home Loans Interest Rates

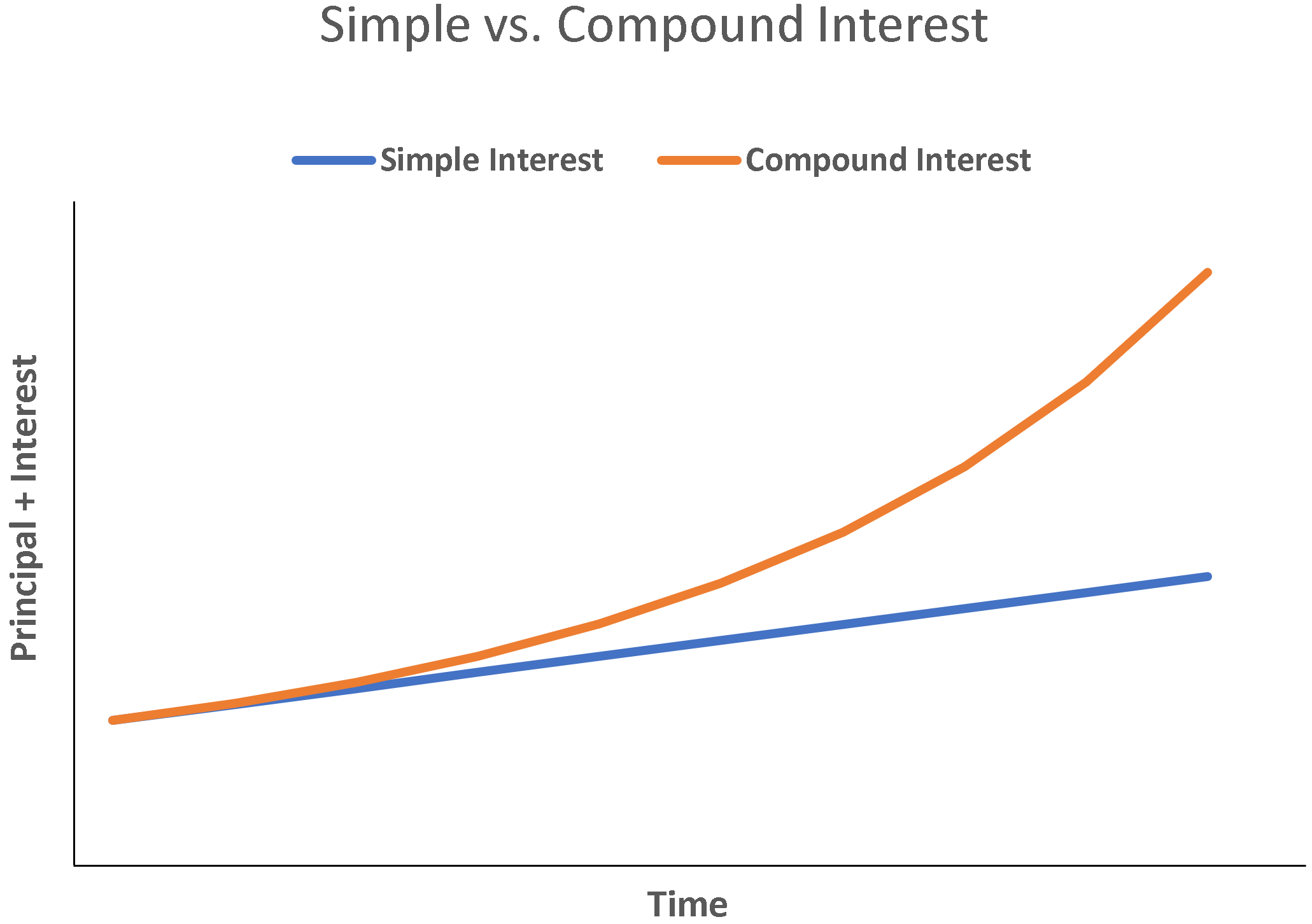

Simple Interest Non Compounding Interest Examples And Formula

First Rate Laminate Wood Flooring Vs Carpet That Will Blow Your Mind Modern Kitchen Flooring Flooring Wood Floor Bathroom

Zero Interest Rate Policy Wikipedia

Cit Bank High Yield Savings Account Earn Up To 2 45 Apy Savings Account High Yield Savings High Yield Savings Account

Low For Long Interest Rates And Banks Interest Margins And Profitability Cross Country Evidence Sciencedirect

Floor Covering Weekly 20 20august 20 2018 20 20picture Perfect Floor Coverings Picture Perfect Perfection

P Jnq63 Qpiclm

Source : pinterest.com