Interest Rate Caps Floors And Collars

An Introduction To Caps Floors Collars Swaps And Swaptions Lancaster Pollard

Difference Between Derivatives Market Finance Investing Investing

How Interest Rate Collars Work Finance Train

Rate Cap Swap And Collar A Cheat Sheet To Managing Rate Risk Derivative Logic

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

Interest Rate Caps And Floors Valuation Finpricing

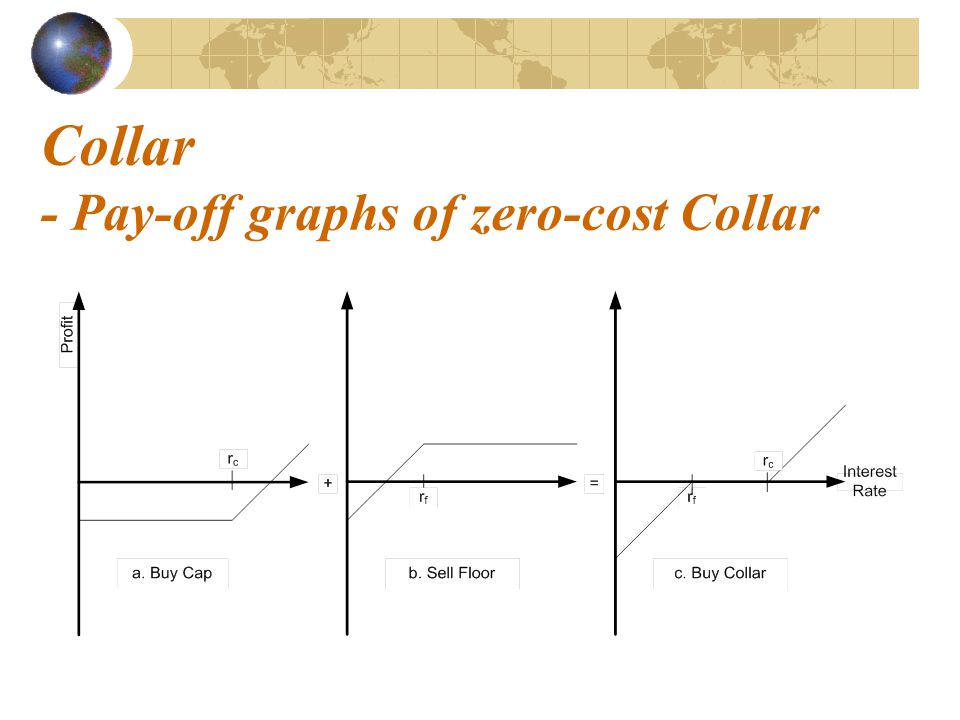

This creates an interest rate range and the collar holder is protected from rates above the cap strike rate but has forgone the benefits of interest rates falling below the floor rate sold.

Interest rate caps floors and collars.

Using Caps And Floors Support Center

Caps Floors And Collars Ppt Download

Multi Period Options Interest Rate Caps Interest Rate Floors Ppt Video Online Download

:max_bytes(150000):strip_icc()/strategy-4086857_19201-23485cf7c4bf4dbbb95c93f267285f16.jpg)

Interest Rate Collar Definition

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

Derivative Market Being An Important Aspect In The Share Market Can Now Be Traded In Online Religare Online Derivatives Market Teacher Life Online Trading

Options Caps Floors

House Plan 3125 00013 Modern Farmhouse Plan 2 556 Square Feet 3 4 Bedrooms 4 Bathrooms Modern Farmhouse Plans Farmhouse Plans House Plans

Dad Hat Or Dad Cap Template Dad Hats Dad Caps Hats

Pin By Joe Mcfarland On Machine Shop Interesting Drawings Blueprints Technical Drawing

Cece Marrakesh Lace Ditsy Print Ruffle Cap Sleeve Top Floral Ruffle Top Bohemian Shirts Cap Sleeve Top

Dog Training A Great Dog Training Tip Is To Make Sure You Understand Other Dogs Are Present When You Puppy Socialization Service Dog Training Puppy Checklist

Via Milavdripclub Air Jordan 1 Low Sb Unc In 2020 Sneaker Outfits Women Red Sneakers Outfit Cap Outfits For Women

Pin By Rebecca Welch On Things Cheongsam Fashion Vocabulary Qipao

Source : pinterest.com